Mark Covell (financial planner and American Airlines pilot) and Kevin Gormley (CFP®, CPA, PFS) discuss the financial implications of the salary increase that comes when pilots get promoted from First Officer to Captain ("left seat").

________

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this video will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 12/06/2022 and are subject to change at any time due to the changes in market or economic conditions.

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses”

- Jerome Powell, August 26, 2022

Upon utterance of these words the equity markets promptly tanked ending the day with a cascade of selling and the S&P500 finished down over 3%. The selling continued over the next several days. Some have jokingly been referring to the Fed Chief as “President” Powell as the markets currently care little about anything else other than analyzing every word he utters for any hint as to whether theFed is dovish (lower interest rates) or hawkish (higher interest rates).

Well, after hearing the above quote, market participants deemed this to be hawkish, which means it was time to sell. News reporters seemed to think the markets were waiting for a sign from the Fed that they were going to back off the rate hikes they have indicated are coming. Why they would think that when inflation (CPI) is currently running 9% year over year is beyond me. We want the Fed to raise rates. Let me explain.

There is no greater drag on our collective financial futures than inflation. Even more than higher taxes or investment fees. Over the last 50 years (Aug 1972-Aug 2022), the S&P 500 has returned a nominal 10.5% CAGR (Compound Annual Growth Rate) with dividends reinvested. After adjusting for CPI, that figure drops to 6.3%. The difference in real dollar amounts is staggering. After 50 years, a $1,000 investment turned into $147,269. However, in purchasing power terms this only increased to $21,215!

The average CPI over this time period was very close to 4%. Think about what 9% would do to our hard-earned dollars over any extended period of time. I want the Fed to keep raising rates, even over 4%, if necessary. Monetary policy(Fed actions)got us into this(along with some fiscal stimulus) and now must get us out. If the Fed needs to induce a recession to get inflation down, so be it. The equity markets will likely recover, and we will be much better off in the long run with lower inflation. The S&P 500 is down 20% YTD as of this writing, what if the recession is already priced in? On the topic of interest rates, I’ve had a number of clients and friends inquiring about whether they should wait for mortgage rates (currently ~5.9%) to decrease before they buy. To be blunt, this makes little sense. As mortgage rates go higher, housing prices must come down (at least on a nationwide basis). The vast majority of homes are purchased with a mortgage, and there is an upper limit on the payments that households can afford. Always remember that the maximum mortgage amount a bank will lend you is based on the monthly payments and their relation to your income, not the home price or interest rates. For example,a $500,000house with 20% down requires a $400,000 mortgage. At 3%, P&I on this home is $1,686per month. At 6%, this jumps to $2,398/month, a 42% increase! To keep payments at the original $1,686/month, the maximum mortgage amount would drop to $281,200.Combined with the original $100,000 down payment, this suggests a home price of $381,200, a decline of over 20%!

I think this is very realistic, particularly in areas of the country with the highest appreciation over the last few years (think Texas, Florida, and Nevada). The bottom line is you are much better off with cheaper property at a higher interest rate than the other way around. You can always refinance later if rates come back down. If you find a house that you can afford and plan to live in for at least ten years, I wouldn’t be concerned about the interest rate but instead, focus on the purchase price.

Important Information:

Leading Edge Financial Planning LLC (“LEFP”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where LEFP and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at www.leadingedgeplanning.com.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

We often talk about behavioral biases, and we are constantly trying to better understand behavioral finance and behavioral economics to make better decisions. We think it’s fascinating because it can have a huge impact on our investment returns, saving habits and therefore our success in retirement.

Another one of the things that it affects tremendously, believe it or not, is taxes. So how does paying taxes drive our behavior?

First, let me talk about behavioral biases. What do we mean by behavioral biases? Certain parts of our brains are wired to make snap decisions to help save our lives, and sometimes this quick thinking really does save your life. What I’m referring to is the limbic system. This system is the emotional center of the brain that takes over under stress. The limbic system is the part of the brain involved in our behavioral and emotional responses, especially as it pertains to behaviors we need for survival, feeding, reproduction, caring for our young, and fight or flight responses.

This system has no doubt led to our advancement and survival as a species, however it often fails when tasked with evaluating certain complex scenarios we face in modern society, especially those that are highly emotional such as our finances.

So, what I wanted to do is address some of the weird things we do as taxpayers to avoid paying taxes.

Of course, there’s nothing wrong with minimizing your taxes. We don’t want to pay one cent more than we’re legally required to, on the other hand, we don’t want to reduce our net worth just to minimize taxes. Unfortunately, that’s what happens a lot of the time.

My father-in-law owns a lake house here in the Knoxville, Tennessee area. The house is paid off and it has appreciated significantly in value over the years. It’s a beautiful place, but they don’t want it anymore. It’s a lot of work for them to properly maintain. So, maybe selling the property would bring them more peace of mind and less stress in retirement. However, he won’t sell it. The primary reason is because he’ll have to pay taxes.

What other ways has the tax aversion bias changed our behavior? Taxfoundation.org has a great article on some of these examples of tax aversion bias.

Have you been to Charleston, South Carolina and noticed that the buildings are narrow and close together? That design started in Amsterdam and was copied around the world. The buildings were intentionally built to be narrow because… you guessed it, taxes. In the 16th century, buildings in Amsterdam were taxed by the width of the property’s façade and how much street frontage they took up.

Real Estate Investing

Another fascinating example from Paris, is the design of the Mansard-style roofs. Architects actually created rooms above the roof line because taxes were levied on the number of floors below the roof line.

Mansard Roof

One of these behaviors that I struggle with and think about a lot is farm equipment. I’d like to buy a new tractor and I know a lot of you probably would too. Tractors are fun! That’s why towards the end of the year I hear folks say, “Hey, I need to reduce my taxes, so I’m going to go buy a tractor. Maybe even a bigger tractor!”

Again, if you need the tractor or farm equipment, that’s a different story, but don’t do things simply because it’s a tax savings. As my business partner, Kevin Gormley will tell you that’s the “tax tail wagging the dog”.

In summary, taxes are a very emotional issue, and this can affect our behaviors. Sometimes we let our emotions make decisions for us, such as the example where I’m not going to pay taxes no matter what or as little as possible no matter what. Just be aware that even though its painful, sometimes it might be smarter to just pay that tax.

Thank you for reading. Please reach out to us anytime. Leadingedgeplanning.com, My email is Charli@leadingedgeplanning.com. We’d love to hear from you!

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this video will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 09/06/2019 and are subject to change at any time due to the changes in market or economic conditions.

“My neighbor invested all of his portfolio in TESLA and now I’m envious! It feels like I’ve FOREVER missed out. And Imight have less money in retirement because I missed the hot stock, ETF, Mutual Fund, etc.?”

“As an investor, you get something out of all the deadly sins—except for envy. Being envious of someone else is pretty stupid. Wishing them badly or wishing you did as well as they did—all it does is ruin your day. Doesn’t hurt them at all, and there’s zero upside to it."

"If you’re going to pick a sin, go with something like lust or gluttony. That way at least you’ll have something to remember the weekend for.”

Warren Buffett

We understand these concerns andfeelings because we’re investing for retirement too! Furthermore, as investment advisors we hear these concerns almost every year. If you’re a diversified investor, there will always be an asset class, a high-flying stock or mutual fund that has higher returns than your diversified portfolio.

Does this mean we’ll have less money for retirement than our neighbor who’s ONLYinvestment last year was TESLA? Historical evidence saysyou’ll likely do just as good or better over the long-term.The “over the long term” part of the sentence presents the challenges. In other words, it’s really hard to be a long-term investor when it feels like the world is falling apart around you AND yourdrinkin’ buddies are killing it with their daily newsletter stock picks!

We all feel the pressure (envy) of missing out ongreat investments that we should have known were going to do better than all the others. The good news is that diversification still works. It’s never really “cool” nor does it ever feel great. However, we believe, and the evidence supports the fact that your chances of success are better in the long run. Check out the numbers from the chart below from BlackRock.

Take a look at our short video where Charlie discusses what it was like in 2020 as investor. How challenging it can be to stay the course and not chase recent returns. Furthermore, the difficulties of feeling like you’ve forever missed out if yourreturns weren’t as high as your neighbor who invested in TESLA, Bitcoin, etc.

Thank you!

Charlie & the Team at Leading Edge Financial Planning

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this video will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 03/12/2021 and are subject to change at any time due to the changes in market or economic conditions.

As we near the end of another year it is always wise to review your financial situation – especially after a year like 2020! Leading Edge has created a checklist to help you evaluate your progress, maximize opportunities, and set goals for 2021. Take this opportunity to do a quick financial self-assessment. Did you meet your financial goals? Did you pay off the debts that you hoped to? Did you keep within your budget? If not, commit to making those changes for the upcoming year.

As always, we are here to help. Please reach out if we can help answer any questions or concerns. Schedule your free consultation today, 865-240-2292

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this document will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 12/23/2020 and are subject to change at any time due to the changes in market or economic conditions.

Not even Hollywood writers could have created a story like we lived out in2020.In this video, Charlie Mattingly and one of Leading Edge’s newest advisors, Rob Eklund,discuss what this year has taught us, howtobetterprepare in the future,andthoughts about the markets and economy going forward.

Leading Edge financial advisor Rob Eklund, aFirst Officer for a major airlineand a retired Air Force Pilot, reviewwhat investors can learn from mission planning in the Air Force and airlines.For example, how can we be proactive instead of reactive? Many times, people may remark how pilots need quick reactions to be successful. As Rob and I know, ifyou arefrequentlyreacting as a pilot,it’s a good indication you did notplansufficiently.We believe it’s the same withinvesting and retirement planning.

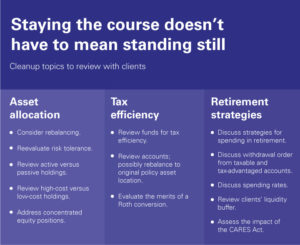

Although, it is to prepareprior to a recession or market downturn, there are many things we can do during the event itself. Vanguard posted the following graphic listingjust a few of the value-added strategies that are critical to consider during any market decline.

In addition to the checklist above from Vanguard, we believe there are ten essential principlesto help all of us remained focused and less stressed during the next market downturn or recession.

Embrace the efficiency of the markets in the long term.

In the short term,the stock marketreflects investor phycology (and many other unpredictable factors).However, over time, equity prices tend to represent the future cash flows of a business. We can all share in those future profits if we have the discipline to remain invested.

Don’t try to outguess the market.

Although there is some debate within the finance community on the exact level of impact on investment returns,most will agree that strategic asset allocation and the amount of time in the market (not market timing) have the most considerable influence on investor returns.

Resist chasing performance.

Do not select investments based on past returns. Funds that have outperformed in the past do not always persist as winners in the future. Past performance alone provides little insight into a mutual fund or ETFs ability to outperform in the future.

Let markets work for you.

The financial markets have historically rewarded long-term investors.We have the opportunity to earn an investment return that outpaces inflation by supplying capital to the companies we invest in. (I.e., stocks, mutual funds, exchange-traded funds)

Consider the drivers of returns.

Evidence shows that buying investments at a fair price (value factor), buying companies that demonstrate a consistent trend of profitability (profitability factor), and companies that tend to be smaller (small-cap premium)point to differences in expected future returns.

Practice smart diversification.

Diversification helps reduce risks that have no expected return. Global diversification can prove beneficial over the long term while reducing the short-term volatility of a portfolio.

Avoid market timing.

You never know which market segments will outperform from year to year. Time in the market is much more profitable than attempting to time the market.

Manage your emotions.

It’s challengingto differentiate the short-term ups and downs of the marketfromthe long-term returns needed to outpace inflation. In reality, themost significantrisk we face is losing purchasing powerover the long-term,during retirement, versus the risk of short-term losses in the market.

Look beyond the headlines.

There will ALWAYS be a news headline that could prevent you from investing in the stock market.The news headlines will either attempt to scare you out of the markets or lure you into the latest investing trend. Either strategy increases viewership,whichin turn sells more commercials.

Focus on what you can control.

As we mentioned at the beginning of the article, just like pilotsplan for their missions in greatdetail, we believe thorough planning is the best way to ensure a successfulinvesting experience plus a fulfilling and prosperous retirement.

Please don’t hesitate to call or email us anytime. We’d love to hear from you!

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this video will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 12/18/2020 and are subject to change at any time due to the changes in market or economic conditions.

As a brand-new pilot, one of the first things you learn is how to mitigate the risk of the potentially deadly physiological phenomenon known as spatial disorientation or spatial-D. In pilot speak, spatial-D is when your body is telling you one thing and your flight instruments (and airplane) are telling you something completely different. Sadly, spatial-D has claimed the lives of many pilots.

In this video, one of our newest Leading Edge team members and previous Marine F/A-18 fighter pilot, Mark Covell discusses just one example of spatial-D. Mark shares how carrier pilots tend to feel like they are pitching up as they are launched off the carrier at night due to the massive acceleration from the catapult. During daytime, VFR conditions this is probably a non-issue. However, in weather, or at night, this type of spatial-D is potentially deadly.

What does spatial-D have to do with investing and retirement planning? Personally, I feel like all of 2020 could be compared to being catapulted off a carrier at night and not knowing what is up or what is down.

During the heat of the battle from February until the markets settled a bit in early April, investor emotions were all over the place. Years of stock market gains evaporated in days, even hours. Furthermore, many people thought, and the news media quickly suggested we were headed for the second Great Depression. And don’t get me wrong, anything was (and is) possible. Sometimes, the unknown can be truly scary.

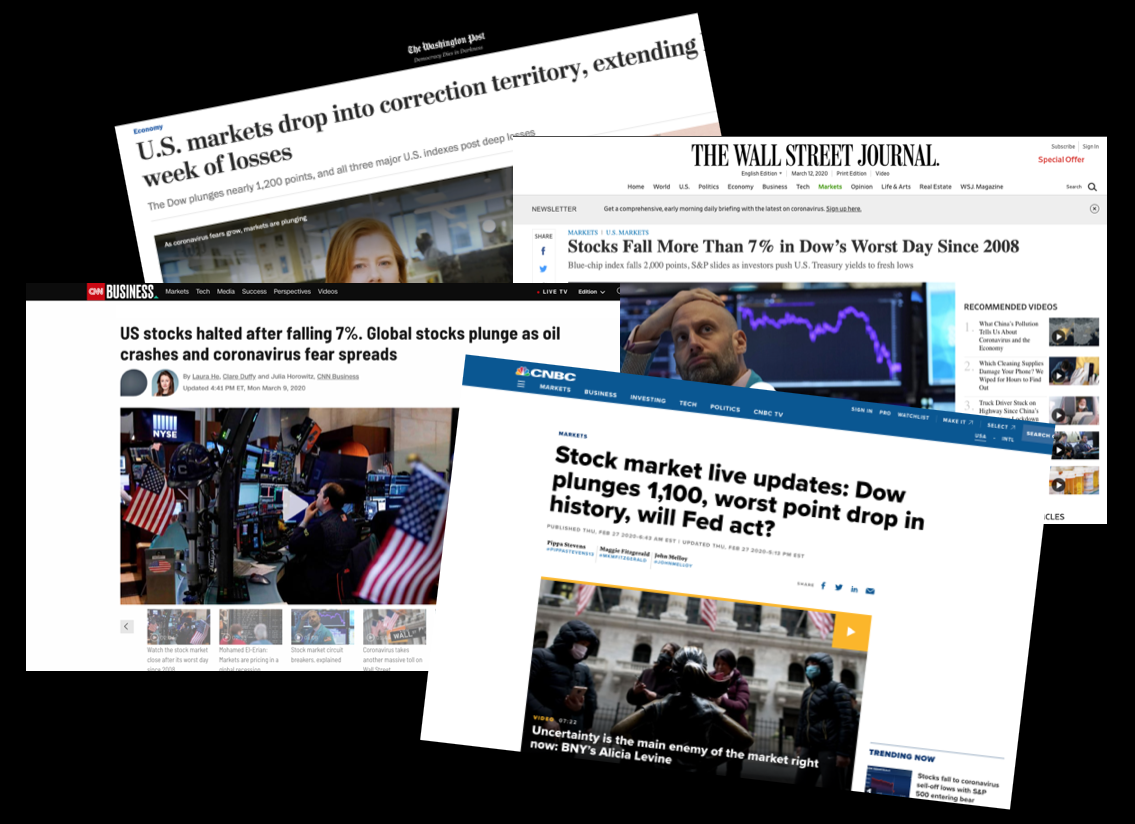

One slightly humorous example of investor spatial-D was early in the pandemic when the shares of ticker symbol ZOOM shot up due to investors buying up shares as quickly as possible. Zoom Technologies, a so-called penny stock had risen more than 240% in the span of a month before the SEC suspended trading. Unfortunately, the traders failed to realize the ticker symbol ZOOM did not represent the Cloud Video Conferencing company Zoom they thought they were purchasing – Ticker symbol ZM.

Here is the headline from MarketWatch.com dated February 27, 2020.

In the airplane, pilots must fight spatial-D by cross-checking and TRUSTING their instruments. If, as an investor, you did not trust your instruments during 2020, it may have been very costly.

So, it’s a dark night and the weather is terrible. What are the instruments you trust? What is your primary and backup instrument? Here are four instruments that I think can save your investments as well as your financial sanity during uncertain times…

1. Cash reserves – Emergency Funds.

Having extra cash can prevent withdrawals from retirement accounts or excessive credit card debt in emergencies. Studies also show having cash in a bank account makes people happy. In an article posted on PYMNTS.com, “Can Cash Really Make You Happier”, Joe Gladstone, research associate at the University of Cambridge in the U.K. and co-author of two recent studies about money and happiness said,

“We find a very interesting effect: that the amount of money you have in your bank account right now is a better predictor of happiness than your aggregate wealth,” Gladstone explained. “Having more money in their bank account makes people feel more financially secure, which leads to an increase in happiness.”

2. Have a working knowledge of financial history.

You don’t have to be an expert or financial historian, but I believe being familiar with financial history is akin to training before you go on a flying mission. Pilots call this chair flying. Athletes and musicians use a technique called visualization that helps them prepare for uncertainty and reduce anxiety for a sporting event or concert.

3. Admit that times are scary, and you do not know what’s going to happen.

This may sound silly, but I’ve seen many people get themselves into a “square corner” because they assumed that something was going to happen when in fact there was no indication or possible way of knowing what the future may hold. We have heard investors say “my gut tells me…” many times.

Some of the best investors in the world invest with the mindset of preparing to be wrong. That’s why diversification is not popular or “sexy” because it’s like admitting you don’t know what’s going to happen in the future, so you must prepare for multiple scenarios. However, diversification can feel disappointing but prove to be a profitable strategy over the long term.

BlackRock Investment Management Company posted the graphic below on their investor education website about diversification and “S&P Envy” over the last 20 years.

4. Prepare and Plan by having a clear vision of your goals and priorities.

If you don’t understand the “why” behind your investments as well as why you’re investing and saving in the first place, you will most likely bail-out of your plan during difficult and uncertain times. Changing your investment plan mid-crisis creates a very high likelihood that your investment returns will be significantly lower.

Simon Sinek started a movement by encouraging businesses to “Start with Why.” It’s a powerful mindset that leads to trust, inspiration and success. I believe the same applies to your financial and investment game plan.

5. Remember that you are invested in companies – not politics.

Sometimes our politics clouds the investment and retirement planning picture. This rule falls under the axiom; “control the controllable.” If you’re allowing your politics to affect your investment game plan than you may want to see rule number 2 above.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this video will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 12/09/2020 and are subject to change at any time due to the changes in market or economic conditions.

You may be the type of person that enjoys managing your own investments. And there’s nothing wrong with that. However, as you approach or are in retirement things can be very different. In fact, when your investment goal switches from accumulation to producing retirement income it may seem as though everything is different now!

In this video, Kevin explains why managing your own investments is different when you are retired, and why a fiduciary financial planner may be worth the investment.

Key Points:

We believe a globally-diversified investment approach is still the best plan for capturing positive returns in the long run. Furthermore, chasing the top-performing asset classes and changing your portfolio based on news headlines or current events has been shown to produce lower returns over the long run. In other words, if you find yourself wanting to change your portfolio as soon as investment headlines turn negative, having a fiduciary financial planner may help you stay focused on your goals instead of abandoning your investment plan during a downturn.

Whether you manage your investments yourself or you have a trusted advisor, here are three things everyone should do to increase your chances of success in retirement.

Write down an Investment Policy Statement to help you stay focused on your investment goals when everything in the news is negative.

For example; “I will invest this way to reach my goals in retirement….”

Be careful chasing the high performing asset classes.

A diversified portfolio should stay diversified.

Have someone who will hold you accountable in order to help you focus on your long-term goals when the going gets tough.

We appreciate your feedback! Please leave a comment on the video or reach out at https://www.leadingedgeplanning.com/ if you have any thoughts on the video!

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this video will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 10/31/2020 and are subject to change at any time due to the changes in market or economic conditions.

It’s tempting to abandon your financial plan when the world is experiencing unprecedented circumstances. Although the pandemic is new and scary, don’t let the headlines play on your fears and knock you off your path.

History shows that recessions and recoveries are filled with short term spikes and falls. These short term events often serve as a distraction to our long term goals. Having a financial plan and sticking with it through the ups and downs has proven time and again to give you the best chance of success.

In truth, the greater potential danger to our financial plan is not the pandemic and market volatility – it’s inflation (the loss of purchasing power in the future). If you react to the headlines and lock in your losses by withdrawing from the market you are also pulling your money from the opportunity to keep up with inflation and therefore, running out of money in retirement.

Stand firm and trust your plan. Feeling unsure? Give us a call, 865-240-2292.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this video will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 05/06/20 and are subject to change at any time due to the changes in market or economic conditions.

Who could have imagined we would start with the spread of a virus, add in some political election turmoil, and now we have an OPEC price war. Wow!

Although we can’t control viruses and oil price wars, there are many things we CAN do to prepare for this bear market or recession. Here are five things to do in order to not freak out and bring peace to your financial life:

1. STOP WATCHING THE NEWS AND START READING IT.

It’s important to be informed. However, the 24-hour news cycle, selling fear and anxiety, is at an all-time high. Instead of watching TV or sensationalized videos, read your news from reputable sources. This will help reduce your emotional reaction while helping you stay knowledgeable and informed. Call us if you would like suggestions of reputable sources.

2. EVALUATE YOUR PERSONAL BUDGET & BALANCE SHEET.

For those of you that have very low debt and a sufficient emergency fund, you can rest easy. Even if you’re laid off or furloughed you will have sufficient cash to prevent you from raiding your retirement funds. If this is not you, consider the following:

● Develop a spending plan to eliminate all short-term, high-interest debt as soon as possible. ● Refocus your spending on necessary items only. ● Increase your emergency savings through automatic payroll deductions. ● Avoid new purchases unless cash is available.

3. CONSIDER A REFI ON YOUR MORTGAGE.

A good friend, and client, recently refinanced his mortgage to a 15-year 2.56% interest rate. This past week we saw mortgage rates fall to the lowest level in almost 50 years. That’s a game-changer for retirement planning!

4. STAY IN THE FIGHT.

You don’t have to be invested in 100% equities all the time, but staying in the market in some capacity is required to capture the long term market gains that are available to all of us. It’s been shown that leaving the market only to return later may diminish your returns significantly. In fact, if you miss out on just a few of the positive days in the market, your long-term stock averages could suffer tremendously. You have to manage risks in the stock market – not avoid them completely.

The chart below shows how $10,000 invested in the S&P 500 index, for the 20-year period of 1999 through 2018, would have performed under various scenarios.

5. FOCUS ON YOUR GOALS & YOUR INVESTMENT TIME HORIZON.

Remember, the money you will need in one to five years is not at risk in stocks. It’s only a paper loss until you sell the stocks. You wouldn’t sell your house or rental real estate property just because the price declined so why would you sell your stocks? Furthermore, more conservative portfolios recover faster from downturns than aggressive ones. For example, according to Charlies Schwab, a portfolio with more than 70% stocks and the rest in bonds took more than two years to recover from the 2008 financial crisis, compared with just seven months for a portfolio with more than 70% in bonds and the rest in stocks.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 03/12/2020 and are subject to change at any time due to the changes in market or economic conditions.